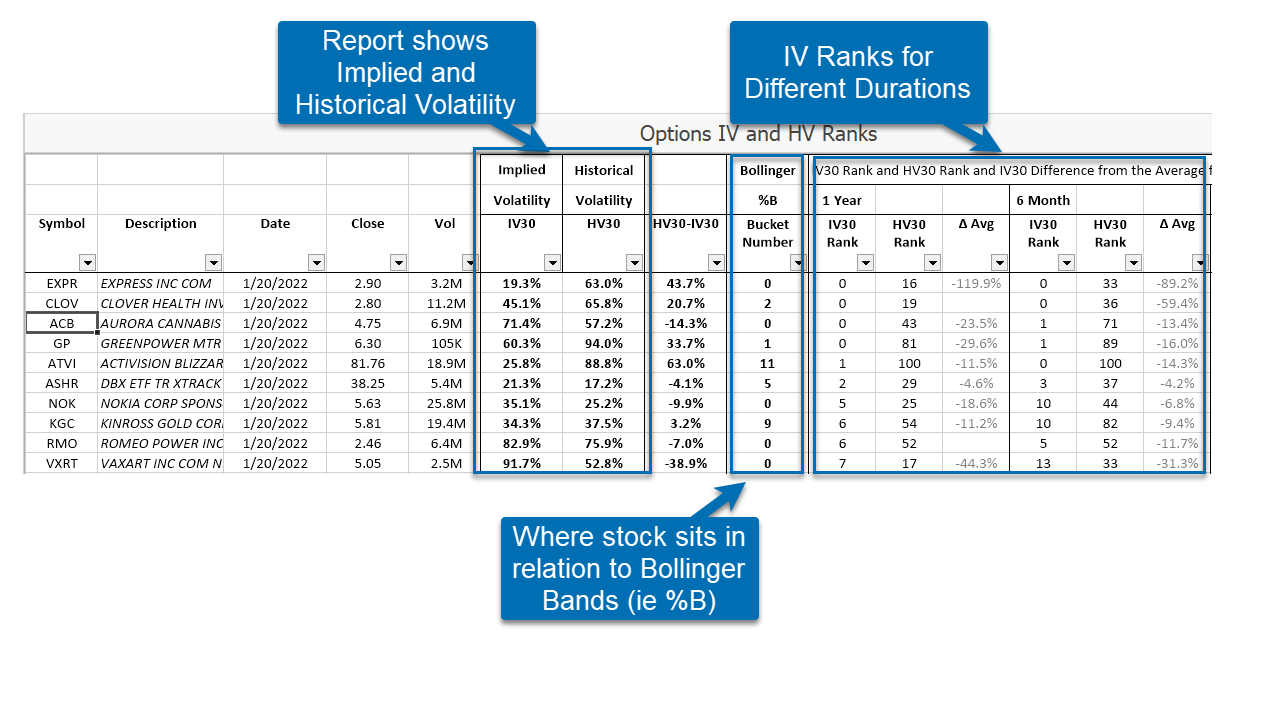

Report shows Implied and Historical Volatility (IV and HV)

And the rank of IV and HV over different lookback periods

And where the stock is currently in relation to Bollinger Bands

For every stock in your symbol list

Report is linked to a chart

Clicking on a symbol

Shows a chart

Configured with Implied and Historical volatility indicator

Template Description

This template produces a report showing current 30 calendar day Options Implied Volatility (IV30) for each stock along with a ranking number indicating whether the IV is low or high when looking back over various periods. The report also show corresponding 22 bar Historical Volatility (HV22) and ranking. 22 Bars is approximately equivalent to 30 calendar days accounting for weekends.

NOTE: This template uses EdgeRater data which includes IV30 data for the entire CBOE Weeklies list.